Stablecoins were supposed to be a crypto side story. A convenience tool for traders who wanted to park dollars between trades without leaving the blockchain.

That’s not what happened.

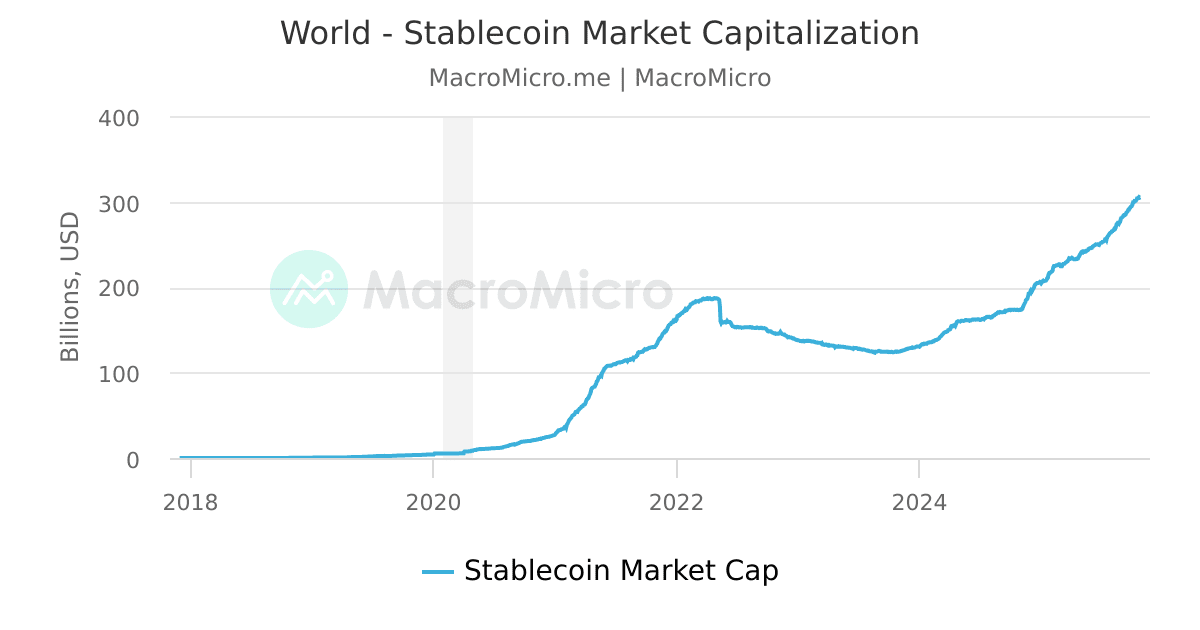

Today they move hundreds of billions of dollars, underpin large portions of crypto liquidity, and increasingly look like a new layer of financial plumbing. And that’s exactly why the regulatory fight in the United States has become so intense.

The official conversation tends to orbit familiar themes: consumer protection, systemic risk, financial stability. All valid.

But there’s another issue hiding in plain sight. Regulatory uncertainty isn’t just constraining crypto firms. It may be putting banks themselves at a strategic disadvantage.

And ironically, those banks may be the institutions best equipped to run stablecoin infrastructure safely.

Banks Didn’t Ignore Stablecoins — They Prepared for Them

There’s a persistent narrative that traditional finance got caught off guard by digital assets. That’s convenient. It’s also wrong.

Several major banks have already built large chunks of the infrastructure required to support tokenized money.

- JPMorgan Chase launched the Onyx blockchain payments network for institutional settlement.

- BNY Mellon rolled out digital asset custody services for institutional clients.

- Citigroup has been experimenting with tokenized deposits that represent bank liabilities on blockchain rails.

None of that was cheap. These projects required new compliance frameworks, custody systems, settlement rails, and operational controls designed to satisfy regulators.

In other words, the plumbing already exists.

The problem isn’t technology.

It’s permission.

The Classification Problem Freezing the System

Right now regulators still haven’t answered a deceptively simple question: what exactly is a stablecoin?

Depending on the answer, the entire regulatory structure changes.

If stablecoins are deposits, banks must apply deposit regulation and capital rules.

If they’re securities, broker-dealer frameworks kick in.

If they’re something new — a payment instrument — regulators have to invent an entirely new category.

Until that question is resolved, banks can’t fully deploy what they’ve built.

And inside large financial institutions, that uncertainty matters more than outsiders realize.

The Governance Wall Inside Banks

Banks don’t launch products the way crypto startups do.

Before anything goes live it runs through layers of internal oversight:

- legal teams

- risk committees

- regulatory affairs groups

- capital planning units

- board-level approvals

Every step asks the same question: what is the regulatory exposure?

If the legal classification of stablecoins is unclear, the answer is “we don’t know.”

That’s a non-starter for most bank boards.

So the infrastructure sits there. Built. Tested. Mostly idle.

One executive described the situation bluntly: banks have already spent the money, but their general counsels won’t let them flip the switch.

Crypto Firms Don’t Have That Constraint

Crypto companies operate under a very different set of incentives.

Many were born in environments where regulation either didn’t exist yet or hadn’t caught up. Their governance structures are lighter. Their risk tolerance is higher. Their global footprint allows them to shift operations between jurisdictions.

Operating in gray zones isn’t a temporary inconvenience for crypto firms.

It’s practically the founding story of the industry.

So while banks wait for regulatory clarity, crypto companies keep shipping products.

Yield programs.

Stablecoin lending markets.

DeFi liquidity pools.

Payment rails built on blockchain networks.

Speed becomes a competitive advantage.

And in fast-moving markets, speed often determines who ends up controlling the infrastructure.

The Yield Gap That’s Starting to Matter

Another pressure point is the widening gap between stablecoin yields and traditional bank deposits.

Many crypto platforms offer stablecoin returns around 4–5%. Meanwhile, average US savings accounts still hover below 0.5%.

This difference isn’t new. Banks have always relied on a spread between the interest they pay depositors and the returns they earn from lending and investments.

What is new is how easily capital can move.

Opening a brokerage account or shifting money into money market funds once required paperwork, settlement delays, and friction.

Moving funds into a stablecoin wallet takes minutes.

Once there, the money can flow into lending markets, exchanges, or yield strategies almost instantly.

That kind of mobility changes the competitive landscape.

We’ve Seen Something Like This Before

Financial history offers a useful comparison.

In the 1970s, US regulations capped how much interest banks could pay on deposits. Money market funds emerged as a workaround, offering market-based yields on short-term securities like Treasury bills.

Depositors moved money rapidly into these funds.

Banks eventually adapted, and regulations evolved.

Stablecoins could represent a similar shift — only compressed into digital time.

Money market funds still relied on brokerage infrastructure and traditional settlement systems. Stablecoins operate on digital rails that settle almost instantly.

That changes the speed of capital migration dramatically.

Why Deposit Flight Isn’t Happening — Yet

Despite the yield gap, massive deposit migration hasn’t happened.

Trust still matters.

Institutions value legal certainty, deep liquidity, and operational reliability. Traditional banks provide those advantages in ways that crypto platforms are still trying to replicate.

For many corporate treasurers and institutional investors, stablecoins remain experimental tools rather than core liquidity instruments.

But the margin is shifting.

Tech-savvy users, fintech companies, and globally mobile investors are already comfortable moving funds between financial ecosystems.

For them, stablecoins increasingly look like programmable digital cash, not speculative tokens.

And once people start viewing them that way, comparisons with bank deposits become unavoidable.

Regulation Could Trigger Unintended Consequences

Regulators are understandably cautious about stablecoin yields.

Many current frameworks prohibit issuers from paying direct interest to holders. The idea is to prevent stablecoins from becoming deposit substitutes without deposit protections.

But markets are adaptable.

Even when direct interest is banned, exchanges can generate returns through other mechanisms:

- lending programs

- staking rewards

- promotional incentives

- structured yield strategies

If regulators attempt to close those pathways, the activity may simply migrate into more complex financial structures.

Synthetic dollar tokens — such as those using derivatives to replicate dollar exposure — are already emerging.

These instruments can generate yield through trading strategies rather than reserve assets, placing them outside regulatory frameworks designed for payment stablecoins.

The Offshore Escape Valve

Another possible outcome is geographic migration.

Crypto markets are inherently global. Exchanges, liquidity providers, and token issuers operate across multiple jurisdictions.

If regulatory frameworks become too restrictive in one country, activity often shifts elsewhere.

This has already happened in crypto derivatives trading, where offshore exchanges dominate global volume.

Stablecoins could follow a similar trajectory.

That would create two problems for regulators:

- Reduced visibility into market activity

- Increased systemic risk outside US oversight

Ironically, strict domestic regulation might push the most innovative financial activity offshore.

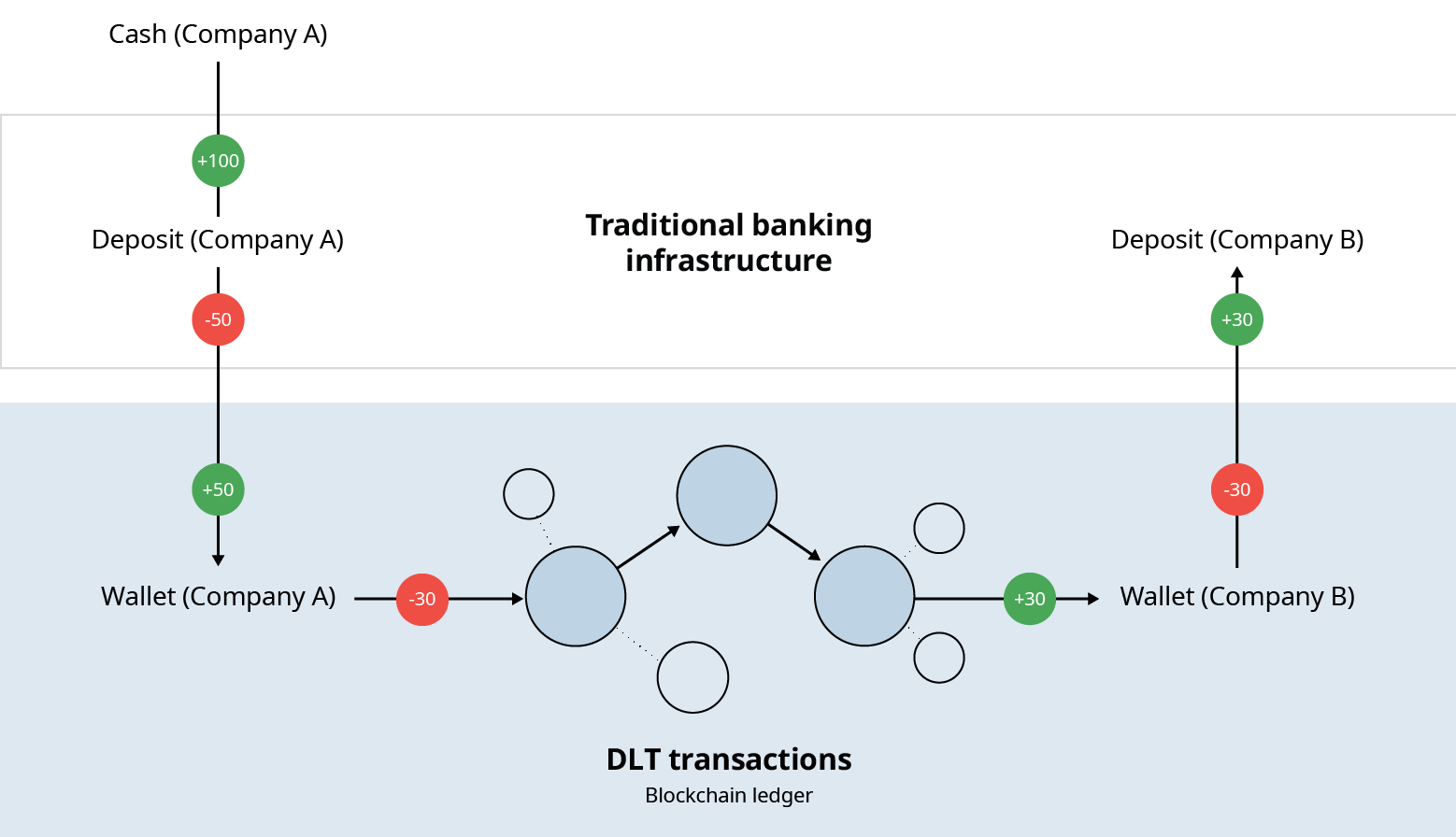

Stablecoins Are Becoming Payment Infrastructure

Beyond yield and trading, stablecoins are quietly evolving into something more foundational: payment infrastructure.

Compared with traditional banking rails, they offer several advantages:

- near-instant settlement

- lower cross-border costs

- programmable transaction logic

- easy interoperability with digital platforms

These characteristics make them particularly useful for international trade, remittances, and digital commerce.

If stablecoins become embedded in global payment networks, the question shifts from whether they exist to who controls the rails.

Banks, fintech firms, and crypto platforms are all competing to define that architecture.

The Strategic Stakes for Banks

For traditional financial institutions, stablecoins represent both a threat and an opportunity.

They threaten the deposit model by making alternative stores of value easier to access.

But banks also possess strengths that crypto companies lack:

- decades of regulatory experience

- sophisticated compliance systems

- trusted brands

- balance sheets capable of supporting large reserve pools

If regulators create a clear framework, banks could become central players in stablecoin issuance and infrastructure.

If uncertainty persists, crypto-native firms may solidify their early lead.

And once infrastructure leadership shifts, it’s difficult to reverse.

The Policy Paradox

The situation creates a strange regulatory paradox.

Policymakers want stablecoins to operate inside a safe, transparent framework.

Yet the lack of regulatory clarity is preventing the institutions most capable of providing that framework — banks — from participating fully.

Meanwhile, crypto firms continue innovating in less constrained environments.

The result is an uneven playing field.

Not because banks lack technology.

Not because they lack capital.

But because governance systems require certainty before action.

The Real Cost of Regulatory Limbo

Stablecoins are no longer a niche experiment.

They sit at the intersection of payments, digital assets, and global liquidity. They already serve as the backbone of large portions of the crypto economy and are increasingly creeping into mainstream financial conversations.

Banks have invested billions preparing for that reality.

But until regulators define the rules, much of that infrastructure remains dormant.

Crypto firms, by contrast, continue building in the open.

In the short term, that dynamic favors innovation outside the traditional financial system.

In the long term, it raises a bigger question: whether regulatory caution designed to protect financial stability could inadvertently reshape who controls the future architecture of digital money.

***

Disclaimer

This article is for informational and educational purposes only and does not constitute financial, investment, trading, or legal advice. Cryptocurrencies, memecoins, and prediction-market positions are highly speculative and involve significant risk, including the potential loss of all capital.

The analysis presented reflects the author’s opinion at the time of writing and is based on publicly available information, on-chain data, and market observations, which may change without notice. No representation or warranty is made regarding accuracy, completeness, or future performance.