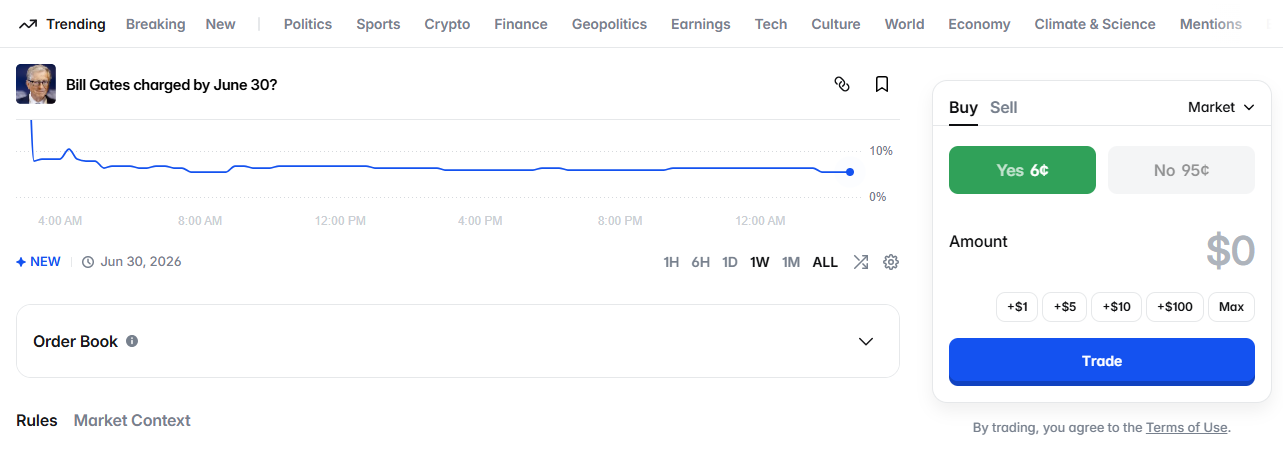

A new Polymarket contract asking whether Bill Gates will be formally charged or indicted in the US by June 30, 2026 is trading around 6% “Yes.”

Six percent.

That sounds dramatic if you’re reading it cold. It isn’t. Not in this context.

What you’re looking at is a long-dated, thin, curiosity-driven market trying to find its opening balance. Not a leak. Not a signal. Not some shadow consensus forming in the dark.

Just tradable uncertainty.

And let’s be very clear about something upfront: the existence of a market is not evidence of wrongdoing. It’s not a claim. It’s a contract with resolution rules and a clock.

Nothing more.

What 6% Actually Means (And What It Doesn’t)

At 6¢, traders are pricing roughly a 6% chance that some US federal or state jurisdiction formally charges or announces an indictment before the deadline.

That’s the full meaning.

It does not imply:

-

guilt

-

likelihood of conviction

-

existence of credible evidence

-

insider knowledge

It’s just a probability price attached to a defined legal trigger.

If you’ve watched enough event markets, you know that 3%–10% is the default “weird things happen” band for long-dated, high-salience names.

Over four months? Strange outcomes are possible. Not likely. But not impossible either.

Markets price tail risk. That’s their job.

Why These Markets Almost Always Open Above Zero

I’ve seen this pattern dozens of times.

Public figure.

Legal outcome.

Multi-month window.

The “Yes” side rarely opens at 0%.

Why?

Because:

-

Some traders buy tiny lottery tickets.

-

Some traders hedge reputational tail risk.

-

Some traders just want optionality exposure.

And early pricing is rarely conviction-driven. It’s liquidity-driven.

In my opinion, 6% here looks like a placeholder number. A soft opening equilibrium while the book is still thin and nobody serious has leaned in.

New Markets Are Fragile

This is the part most casual observers miss.

Newly listed markets are not robust probability engines. They’re shallow pools.

Early on:

-

Spreads are wider.

-

Depth is thin.

-

Last trade ≠ consensus.

-

A handful of traders can move the headline price.

So if you’re reading 6% like it’s a refined forecast, you’re giving it too much weight.

In early-phase markets, price is often just the last person willing to cross the spread.

That’s it.

The Real Signal Isn’t 6% — It’s Behavior

If this contract becomes meaningful, it won’t be because of the number. It’ll be because of how that number reacts to stress.

Here’s what actually matters:

1) Stickiness.

If 6% holds for days with balanced flow, that suggests a stable tail-risk premium.

2) Rumor spikes that fade.

If it jumps to 12% on social chatter and snaps back to 6%, that’s the market discounting noise.

3) Volume-backed repricing.

If it jumps and volume accelerates — and price doesn’t retrace — then something changed.

In prediction markets, follow-through + size is the difference between signal and noise.

Everything else is theater.

Let’s Look at the Book (Because That’s Where the Truth Is)

At first glance:

Last trade: 6¢

Spread: 1¢

Implied probability: ~6%

Looks tight. Efficient.

It’s not.

Once you examine the depth, you see what this really is: a low-conviction, liquidity-fragmented book.

The Asks (Selling “Yes”)

7¢ → 505 shares

8¢ → 91 shares

9¢ → 1,316 shares

10¢–14¢ → thin

There’s no heavy sell wall. No massive size defending 8¢ or 10¢. If someone aggressively lifts $20k–$30k, this thing gaps higher quickly.

That doesn’t mean it should. It means the structure is fragile.

No anchoring. Just resting.

The Bids (Buying “Yes”)

5¢ → ~1,000 shares

4¢ → ~200 shares

3¢ → ~169 shares

2¢ → ~310 shares

1¢ → 3,220 shares

Notice the real size only shows up at 1¢.

That’s not conviction buying. That’s lottery-ticket positioning.

There’s no aggressive bid stack defending 4% or 5%. It’s passive optionality fishing.

Translation: nobody is pounding the table that this is mispriced at 6%.

The 99¢ Wall on “No”

Yes, you’ll see size at 99¢, 98¢, 97¢ on the “No” side.

That’s normal. In binary markets, people farm premium by selling high-probability outcomes.

But those walls don’t tell you much about near-term conviction. They’re structural.

The real information sits in the mid-book. And here? The mid-book is thin.

What This Structure Actually Tells You

This isn’t a conviction market.

It’s:

-

curiosity trades

-

small retail positioning

-

passive premium selling

No strong bid defense.

No heavy sell resistance.

Wide liquidity gaps.

Classic early listing behavior.

In markets with serious institutional belief, you see defended zones and thick layering around fair value.

This isn’t that.

The Built-In Misinterpretation Trap

These markets attract bad takes because people conflate three different things:

“A market exists.”

“A market has a non-zero price.”

“Something must be happening.”

That’s how misinformation spreads.

A prediction market is not a court filing. It’s not investigative journalism. It’s not a leak.

It’s a contract with a timer.

What Would Actually Move This for Real

If this market reprices meaningfully, it will be on something concrete:

-

A credible report of a formal investigation advancing.

-

Documented legal filings.

-

Official statements narrowing uncertainty.

Absent that?

Moves will likely be:

-

rumor-driven

-

social-driven

-

liquidity-driven

And those usually mean-revert.

Time decay is brutal in these contracts. Silence bleeds “Yes.”

Desk-Level Read

What phase is this in?

Early discovery.

Is 6% strong signal?

No. It’s a soft equilibrium in a shallow book.

Is there hidden intelligence implied by structure?

Nothing about this order book suggests that.

Is the market stable?

Yes — but only because no one with size cares yet.

What’s the biggest risk for “No” sellers?

A single credible catalyst can gap price upward fast because the book above 6¢ is thin.

What kills the “Yes” side over time?

Silence. Weeks passing without developments. Sellers leaning into decay.

Right now, 6% looks like what it probably is:

A small, tradable tail-risk premium floating in a thin book while the contract is still young.

Nothing more.

Polymarket Prices a 6% Chance of “Bill Gates Charged by June 30” — But This Is More About Market Design Than “Inside Info”

A newly created Polymarket contract asking whether Bill Gates will be formally charged or indicted in the US by June 30, 2026 is trading around 6% “Yes”. That number looks dramatic at first glance. In practice, it’s often a sign of something less sensational: a low-liquidity, long-dated market finding its opening equilibrium.

This isn’t a market saying “something is coming.” It’s a market saying, “In a world where lots of weird things can happen over 4 months, we’ll price a small tail risk — and we’ll revise it if real information shows up.”

And to be crystal clear: a prediction market listing is not evidence of wrongdoing. It’s just tradable uncertainty.

What “6%” Actually Means Here

At 6¢, the market is implying roughly a 6% probability that some US federal or state jurisdiction formally charges or announces an indictment within the window.

That’s it.

It does not mean:

-

guilt,

-

likelihood of conviction,

-

or that there’s credible evidence behind the rumor mill.

It’s simply the market’s current price for a defined legal event occurring by a deadline.

Why These “Celebrity Legal” Markets Often Open Around 3%–10%

If you’ve watched enough prediction markets, you see the same pattern repeatedly:

-

Long-dated, high-salience questions (public figures + legal outcomes) often open with a non-zero “Yes” even when there’s no concrete catalyst.

-

Early pricing is driven by a mix of:

-

curiosity trades,

-

small “lottery ticket” sizing,

-

and a basic truth: over a multi-month window, improbable events aren’t impossible.

-

In my opinion, 6% here is basically a placeholder price until the market either:

-

attracts serious liquidity, or

-

gets hit with real, verifiable news that forces repricing.

This One Is Especially Vulnerable to Noise Because It’s New

New markets are fragile. Full stop.

Early on, a handful of traders can set the tone because:

-

spreads are wider,

-

the book is thinner,

-

and “price” is often just “last trade,” not deep consensus.

So if you’re reading 6% like it’s a polished probability forecast, you’re giving it too much credit. In the early days, price is often a liquidity artifact.

The Real Signal Isn’t the Price — It’s How the Price Behaves

If this market is going to become meaningful, you’ll see it in behavior, not the headline number.

Here’s what I’d watch:

1) Does 6% stay sticky for days?

Sticky pricing usually means the market found a stable balance between:

-

people buying cheap tail risk, and

-

people selling it as “free yield.”

2) Do spikes fade fast?

If “Yes” pops to 10%–15% on a rumor and then snaps back, that’s the market telling you it’s discounting noise.

3) Do spikes hold and volume follows?

That’s the opposite situation: information may be entering, or at least a cohort believes it is.

The difference between “noise” and “signal” in Polymarket is usually: follow-through + volume.

The Built-In Trap: These Markets Invite Misinterpretation

Markets like this are magnets for bad takes because people conflate:

-

“A market exists” with “a thing is likely,” or worse,

-

“a thing is true.”

That’s how misinformation spreads.

A prediction market is not a court document. It’s not a newsroom. It’s not a leak.

It’s a tradable contract with a defined resolution rule, and traders are buying and selling a tail-risk timeline.

What Would Actually Move This Market for Real

If the market is rational, it should only materially reprice on developments like:

-

a credible report of an investigation that appears to be advancing,

-

legal filings tied to the subject,

-

or explicit official statements that narrow the uncertainty.

Absent that, most movement will be:

-

rumor-driven,

-

social-driven,

-

or liquidity-driven.

And those moves tend to mean-revert.

Desk-Level Take

What phase is this market in?

Early discovery. It’s a new listing trying to find a fair “tail risk” price.

What usually kills the “Yes” side in markets like this?

Time decay plus silence. If nothing concrete emerges, “Yes” often bleeds down slowly as sellers lean on it.

What’s the biggest risk for “No” sellers?

A single credible catalyst can gap price up fast, because these markets can jump in steps when uncertainty flips.

The clean read:

At 6%, this doesn’t look like “inside intelligence.” It looks like a small, tradable tail-risk premium while the market is still young and thin.

What the Order Book Really Says About “Bill Gates Charged by June 30?”

At first glance, the market shows:

-

Last trade: 6¢

-

Yes implied probability: ~6%

-

Spread: 1¢

That looks tight. That looks efficient.

But once you actually inspect the depth, you realize something important:

This is not a conviction market.

This is a liquidity-fragmented market.

1️⃣ The Asks (People Selling “Yes”)

Look at the sell wall:

-

7¢ → 505 shares

-

8¢ → 91 shares

-

9¢ → 1,316 shares

-

10¢–14¢ → very thin

The ladder above 6¢ is not deep.

There is no massive defensive wall at 8¢, 10¢, or 12¢.

If someone aggressively buys $20–30k market orders, this thing can jump several cents quickly.

That means:

The market is not strongly anchored at 6%.

It’s just resting there.

2️⃣ The Bids (People Buying “Yes”)

Now look at the downside:

-

5¢ → ~1,000 shares

-

4¢ → ~200 shares

-

3¢ → ~169 shares

-

2¢ → ~310 shares

-

1¢ → 3,220 shares

Notice something?

Real size only appears at 1¢.

That’s not bullish. That’s lottery-ticket positioning.

The book between 2¢ and 5¢ is shallow relative to the potential tail risk narrative.

Translation:

There is not aggressive belief this should be 3% or 4%.

There is passive willingness to catch extreme cheap prints.

3️⃣ The 99¢ Wall Is Irrelevant

You also see large size at:

-

99¢

-

98¢

-

97¢

That’s the “No” side depth.

That’s normal in binary markets. People are selling “Yes” at high certainty because they believe it resolves No. But those walls don’t tell you much about current conviction — they mostly reflect people farming premium.

The real signal is near the mid-book.

4️⃣ What This Structure Actually Means

This is a low-conviction, early-phase book.

-

No strong bid defense at 6%

-

No heavy sell resistance above 6%

-

Wide liquidity gaps

-

Thin mid-layers

That’s classic new-market behavior.

In markets with real institutional conviction, you see:

-

Thick layers around fair value

-

Defended price zones

-

Clear inventory accumulation

This book looks like:

-

curiosity trades

-

small retail positioning

-

optionality selling

Nothing more.

5️⃣ The Most Important Insight

The 6% price is not being defended by serious capital.

It’s floating in a thin band because:

-

no catalyst exists,

-

no urgency exists,

-

and no large player has decided to lean on one side.

If real information entered this market, price could move fast — not because the probability suddenly changed, but because the book is thin.

That’s the key takeaway.

Desk-Level Read

Is 6% a strong market signal?

No. It’s a soft equilibrium in a shallow book.

Is there hidden intelligence here?

Nothing in the structure suggests that.

Is this market stable?

Yes, but only because nobody cares enough yet.

What would change that?

One credible legal development or high-confidence investigative report would:

-

Blow through 7–10¢ instantly

-

Trigger FOMO buying

-

Force liquidity to re-layer

Right now, this is a tail-risk premium sitting on autopilot.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial, investment, trading, or legal advice. Cryptocurrencies, memecoins, and prediction-market positions are highly speculative and involve significant risk, including the potential loss of all capital.

The analysis presented reflects the author’s opinion at the time of writing and is based on publicly available information, on-chain data, and market observations, which may change without notice. No representation or warranty is made regarding accuracy, completeness, or future performance.

Readers are solely responsible for their investment decisions and should conduct their own independent research and consult a qualified financial professional before engaging in any trading or betting activity. The author and publisher hold no responsibility for any financial losses incurred.