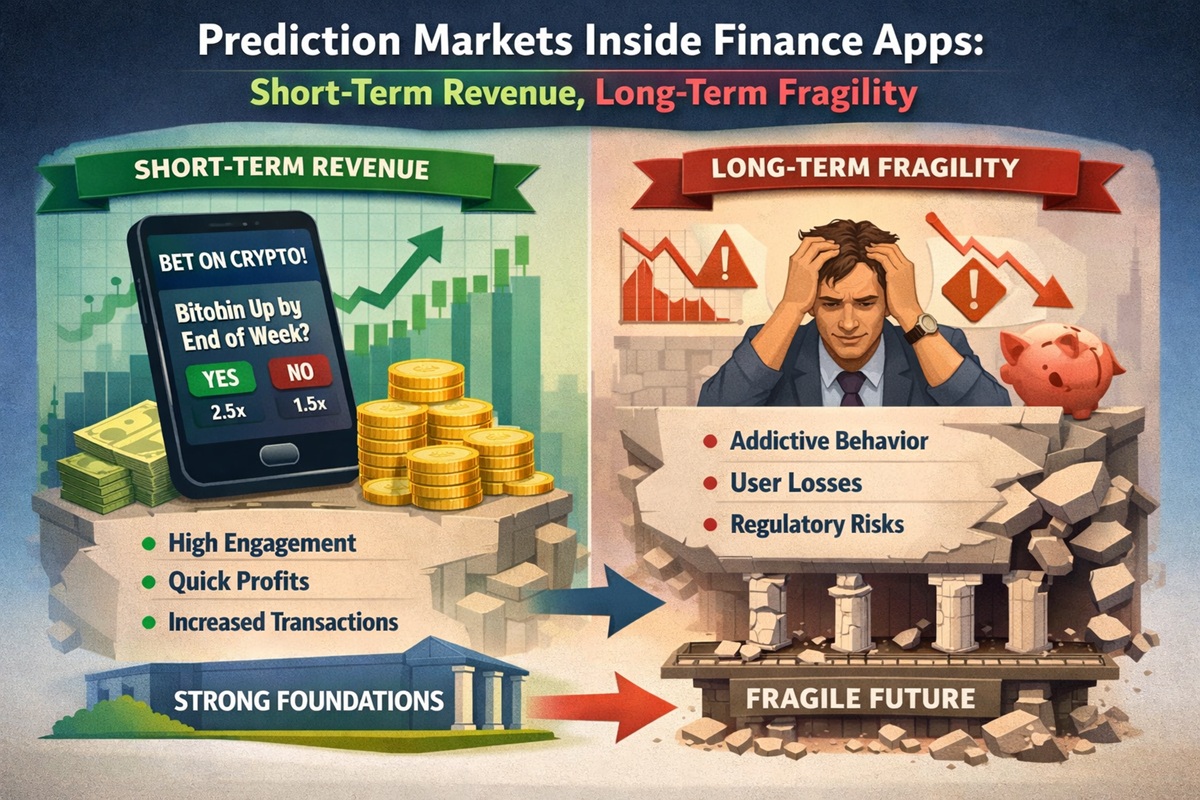

The rapid push by mainstream finance platforms into prediction markets reflects a familiar pattern in consumer fintech: when growth in core products slows, attention turns to higher-engagement, higher-volatility offerings that promise immediate revenue uplift. What is different this time is the nature of the product being introduced — event-based speculation that closely resembles casino dynamics — and the strategic risk this introduces to platforms whose long-term value depends on user longevity rather than transactional intensity.

This tension is at the center of recent criticism from Santiago Roel Santos, founder and CEO of Inversion Capital, who argues that prediction markets, while intellectually compelling and potentially useful as information tools, may undermine the durability of retail finance platforms by accelerating user churn through account liquidation.

His critique arrives as platforms like Robinhood, Coinbase, and Gemini move aggressively to integrate prediction-style products — often via partnerships with regulated event contract providers such as Kalshi. The strategic question is not whether these products can generate revenue, but whether they are compatible with the economics of long-term retail finance.

Why Prediction Markets Are Attractive to Platforms

Prediction markets are seductive for product teams for clear reasons:

-

They generate high engagement per dollar of user capital

-

They monetize attention rather than assets under management

-

They fit naturally into app-based, mobile-first UX

-

They produce frequent resolution events, driving repeat usage

From a platform perspective, prediction markets solve a near-term problem. Traditional retail trading has matured. Equity commissions are compressed, crypto volumes are cyclical, and interest income is sensitive to rate environments. Event contracts, by contrast, produce consistent transactional activity regardless of market direction.

In the case of Robinhood, the appeal is obvious. The platform’s original growth thesis — democratized equity trading — has already been realized. Incremental growth now requires either expanding into more of the user’s financial life or extracting more activity from the same base. Prediction markets fall squarely into the second category.

But this is where Santos’ warning becomes structurally important.

Churn, Not Losses, Is the Real Risk

The core of Santos’ argument is not moral opposition to speculative products. It is an economic critique grounded in customer lifetime value.

Losses alone do not destroy platforms. What destroys platforms is user exit.

In casino-style systems, the probability distribution matters. The longer a user participates, the higher the statistical likelihood that they eventually lose enough to disengage entirely. Unlike long-term investing — where volatility can be absorbed over decades — event-based markets compress outcomes into short timeframes. Capital is either preserved or destroyed quickly.

Once an account is effectively liquidated, the user is no longer a future customer for credit, savings, insurance, or wealth products. From a lifetime value perspective, that user drops to zero.

This dynamic is well understood in gambling economics, but it is less frequently acknowledged in fintech product strategy. Many platforms focus on average revenue per user, while underweighting user survival probability.

Prediction markets optimize for engagement density, not longevity.

The Structural Conflict With Retail Finance

Retail finance platforms are not casinos, even when they occasionally behave like them. Their long-term value depends on:

-

Multi-decade user relationships

-

Gradual balance growth

-

Cross-selling into adjacent financial products

-

Trust, not adrenaline

Prediction markets invert these priorities. They reward rapid turnover, emotional decision-making, and binary outcomes. Over time, this changes not just user behavior, but platform identity.

Santos’ point that “users age” is more than a rhetorical flourish. Financial behavior evolves predictably:

-

Early users seek access and novelty

-

Mid-life users prioritize stability and planning

-

Mature users value risk reduction and liquidity management

Platforms that fail to evolve with their users eventually lose them — either to incumbents or to disengagement. Introducing casino-like products late in the lifecycle risks freezing the platform in its most speculative phase.

Lessons From Crypto’s First Cycle

Crypto exchanges provide a cautionary parallel. During peak cycles, platforms optimized aggressively for leverage, perpetuals, and high-frequency speculation. Revenue surged. User counts ballooned.

Then volatility reversed.

What followed was not just trading losses, but mass churn. Users who lost heavily did not downgrade activity — they exited entirely. Reacquisition costs soared. Regulatory scrutiny intensified. Long-term monetization collapsed.

Coinbase’s renewed interest in prediction markets, framed as part of its “everything app” strategy, echoes this pattern. The risk is not regulatory alone. It is that speculative density crowds out slower, more durable financial relationships.

Information Markets vs. Speculation Engines

It is important to distinguish between the theoretical value of prediction markets and their practical implementation inside consumer apps.

As information mechanisms, prediction markets can be powerful. They aggregate dispersed knowledge, surface probabilistic expectations, and often outperform polls and expert forecasts. During the 2024 US election cycle, event contracts demonstrated notable accuracy in pricing political outcomes.

But information markets become speculation engines when:

-

Position sizes are unconstrained

-

UX emphasizes excitement over probability literacy

-

Products are surfaced to users without risk context

-

Resolution frequency encourages compulsive behavior

Inside mainstream finance apps, these conditions are difficult to avoid. The same UX principles that make trading accessible also make speculation frictionless.

Balance Sheet Strength vs. Franchise Value

One of Santos’ most overlooked points is the distinction between short-term financial performance and long-term franchise strength.

Prediction markets may look attractive on quarterly earnings:

-

Higher transaction counts

-

Increased engagement metrics

-

Strong contribution margins

But they also introduce tail risk at the user level. A platform with impressive near-term metrics but declining user durability is building a fragile franchise.

In contrast, products like:

-

Credit cards

-

Savings accounts

-

Insurance

-

Cash management tools

are slow, regulated, and operationally complex. They are also sticky. They embed the platform into daily financial life. They reduce churn because users cannot easily exit without friction.

These products do not spike engagement. They compound value.

The Superapp Temptation

The “financial superapp” narrative encourages platforms to be everything at once: trading venue, payments app, betting interface, wallet, and lifestyle hub. In theory, this maximizes optionality.

In practice, it often results in incoherent product strategy.

Superapps succeed when adjacent products reinforce the core relationship. They fail when new features cannibalize trust or destabilize user outcomes. Prediction markets risk doing exactly that by introducing negative-sum dynamics into platforms built on positive-sum financial growth.

Regulatory Gravity Is Not the Only Constraint

Much commentary around prediction markets focuses on regulatory risk. While this is relevant, it is secondary to the economic issue.

Even fully regulated, transparent, and compliant prediction markets still carry the churn dynamic Santos describes. Regulation does not change probability distributions. It only governs disclosure and access.

Platforms that rely on regulation as the primary safeguard miss the deeper strategic risk: user extinction events.

A Different Optimization Function

Santos’ conclusion — that platforms should treat churn as a first-class risk — implies a different optimization framework:

-

Maximize user survival, not transaction velocity

-

Optimize for decade-long relationships, not quarterly ARPU

-

Accept lower engagement in exchange for higher durability

This is an uncomfortable prescription in an industry conditioned to chase growth metrics. But history favors platforms that resist short-term extraction in favor of long-term compounding.

Where Prediction Markets May Still Belong

None of this implies prediction markets should not exist. The question is where and how.

They may thrive as:

-

Standalone platforms

-

Professional tools for institutional users

-

Information overlays with capped exposure

-

Research-oriented products rather than engagement engines

What Santos challenges is their placement inside mass-market finance apps whose economic survival depends on users staying solvent, engaged, and trusting for decades.

The Strategic Trade-Off Ahead

As Robinhood, Coinbase, and Gemini move forward with prediction market offerings, the trade-off becomes explicit:

-

Short-term revenue and engagement, or

-

Long-term user value and franchise resilience

These are not easily reconciled. Platforms that choose durability will likely look boring by comparison. But boring products, as Santos notes, are often the ones that work.

In consumer finance, excitement is transient. Relationships are the asset.

[…] people think coins die early.That’s […]